Abstract

This paper constructs various measures of domestic and global uncertainty and provides a comprehensive study of their impacts on the Thai economy. Based on a small open economy VAR, global uncertainty delivers deeper and more long-lasting effects when compared to within-country ones. In addition, we find that uncertainty shocks first generate sudden and large declines for stock prices and foreign portfolio investment, before gradually affecting the real economy through investment and trade channels. There is also meaningful heterogeneity among different types of domestic uncertainty. While financial uncertainty matters most for the Thai economy overall, consumption demand largely responds to macroeconomic uncertainty, while economic policy and political uncertainty generates the most persistent effects on investment. Furthermore, fiscal policy uncertainty is a key driver of trade flows while monetary policy uncertainty plays an important role for capital markets.

Similar content being viewed by others

Notes

In large part, this is due to the lack of long samples and reliable data for these countries. Uncertainty indicators proposed in the literature are also only mainly available for the US and few other developed economies. See www.policyuncertainty.com.

This is a distinction that earlier measures of uncertainty such as survey-based ones often fail to address. First moment shocks can be thought of as a deterioration in the expected outcome which is not uncertainty, just bad news. Second moment shocks on the other hand are uncertainty and are defined as a greater range of expected outcomes. Disentangling the two can be difficult, especially since market participants tend to become more pessimistic in the face of greater uncertainty.

The LDA algorithm involves two main steps. First, for each newspaper article, the process starts by randomly choosing a distribution over topics. In the second step, each word in each document is then drawn from one of the topics, where the selected topic is chosen from the per-document distribution over all topics. In this way, all documents will always share the same number of topics but with different proportions. Readers are referred to Blei (2012) for more details on the algorithm.

These are (i) Bangkok Biz News, (ii) Daily News, (iii) Matichon and (iv) Thairath.

They are in Thai language and are available upon request.

Note that although there are more than five topics in the full corpus, since we choose to discard the remaining topics that cover other uncertainty-related issues such as those on education, the environment, healthcare and housing, we scale the total count of uncertainty-related articles in our five selected topics to 100. In this way, we can focus on analyzing how important each of these five topics are in relation to each other. This is also for visual purposes of viewing Fig. 2, since the number of other uncertainty-related topics that we discard are quite large.

In the literature, the PCA has often been employed to gauge the overall level of uncertainty across a swathe of uncertainty proxies that are often available, and has been shown to capture the common movements among the various indicators of uncertainty well (see Haddow et al. 2013; Forbes 2016 and Redl 2017, among others).

That is, our empirical results are robust to other global uncertainty measures that includes applying the PCA to combinations of the BBD US news-based uncertainty, the Euro area news-based uncertainty and the VIX index as well.

Another popular ordering of the VAR in the literature is one of the reverse orders with uncertainty ordered last. We performed the reverse-order analysis as a robustness check, where the interpretation of our findings did not change significantly. Nevertheless, it is still unclear whether uncertainty should be placed before or after the real activity variable. Also, there is a recent strand of the literature that debates whether the recursive VAR identification approach is a relevant approach at all, given that there may be reverse caUSlity between uncertainty and real activity. Few studies that address this potential endogeneity of uncertainty propose novel identification procedures (Carriero et al. 2018b; Cesa-Bianchi et al. 2018; Mumtaz 2018; Angelini et al. 2019; Ludvigson et al. forthcoming), but so far have delivered empirical results that are quite mixed.

The majority of VARs in the literature that investigate the effects of uncertainty are in levels except for some that consider growth or HP-filtered variables. According to Sims et al. (1990), VARs in log levels provide consistent estimates of the IRFs even in the presence of co-integrating vectors.

Information criterion tests suggest either VARs with 1 or 2 lags, so we select a VAR with 1 lag due to the large number of endogenous variables in the VAR. The results are also robust to VARs with 2 lags. To ensure no model misspecification, we also perform multivariate Portmanteau tests to ensure no serial correlation in the error terms of the VAR models.

We also obtain the impulse responses of inflation and the policy rate to global and local shocks but we do not wish to discuss them here since the Thai CPI and policy rates have been relatively stable throughout the sample under investigation.

There appears to be some minor evidence of overshooting for the impact of macroeconomic uncertainty shocks on consumption and investment (Fig. 5), but is only marginally significant. For studies that find evidence of overshooting, we notice that they tend to use volatile implied or realized financial market volatility measures as proxies for uncertainty, whereas studies that use alternative proxies for similar countries find no such effect (Jurardo et al. 2015; Cuaresma et al. 2019). Thus, the rebound effect may depend on the type of uncertainty measure used. Alternatively, it may depend upon cross-country differences or the sample period under investigation. Carrière-Swallow and Cèpedes (2013) offer evidence that real activity tends to occur in the medium run for developed economies, while emerging economies do not display a similar pattern. Caggiano et al. (2014) show that if the sample period includes the GFC where most developed central banks switched to unconventional monetary policy measures in the presence of the effective zero lower bound, the overshoot vanishes.

Note, however, that not all types of capital flows may react alike to uncertainty. For example, Hlaing and Kakinaka (2019) shows that for 50 developed and emerging markets, global uncertainty clearly increases the likelihood of contractions in FPI for all countries, while it increases FDI in only advanced economies

We also examine the FEVD results at other horizons, but the findings that they deliver do not qualitatively change our discussion of results. Results are available upon request.

To provide a guide for factor estimation, we use the Bai and Ng (2002) information criterion (IC) to select the number of factors. The IC suggests 3 factors which explains only 21% of the variation in the dataset, where the first three factors load heavily on real activity measures such as retail sales and the manufacturing production index, the SET index and return on its components, and government bond rates, respectively. Since the variation explained by the three factors are rather low we also consider extracting 18 factors which can explain at least half of the variation of series in the dataset. However, we find whether using 3 or 18 factors provides aggregate uncertainty measures that are not statistically significantly different; thus, we use 3 factors in our empirical investigation.

Other weighting schemes are also possible such as by employing the principal component analysis (PCA) approach. We follow JLN and construct these measures as part of our robustness checks and find that final indices do not differ significantly.

Similar to JLN, we find that the response of economic variables to macroeconomic and financial uncertainty of various horizons do not differ in a significant way.

We follow Wallach et al. (2009) and calculate the perplexity value as \(perplexity(W) = exp\{ \frac{\sum log P(w_d | \Phi , \alpha )}{\sum N_d}\} \), where W is the test set which contains a random selection of articles \(w_d\) which amount to 10% of all articles in the full dataset. For each article \(w_d\), the probability \(P(w_d | \Phi , \alpha )\) is computed as \(P(w_d | \Phi , \alpha ) = \int d\theta P (w_d | \theta ,\Phi ) P(\theta |\alpha )\), in which the integral is approximated via the iterated pseudo-count method. \(\sum N_d\) is the total number of words in the whole set and parameters \(\Phi \) and \(\alpha \) are learned from the training set.

References

Abel J, Rich R, Song J, Tracy J (2016) The measurement and behavior of uncertainty: evidence from the ECB survey of professional forecasters. J Appl Econom 31(3):533–550

Ahir H, Nicholas B, Davide F (2021) What the continued global uncertainty means for you. IMF Blog, January 19

Alessandri P, Bottero M (2017) Bank lending in uncertain times. BCAM Working Papers 1703, Birkbeck Centre for Applied Macroeconomics

Alessandri P, Mumtaz H (2019) Financial regimes and uncertainty shocks. J Monet Econ 101:31–46

Angelini G, Bacchiocchi E, Caggiano G, Fanelli L (2019) Uncertainty across volatility regimes. J Appl Econom 34(3):437–455

Arbatli EC, Davis SJ, Ito A, Miake N, Saito I (2019) Policy uncertainty in Japan. Hoover Institution Economics Working Papers No. 19109

Arellano C, Bai Y, Kehoe P, (2012) Financial frictions and fluctuations in volatility. Staff Report 466, Federal Reserve Bank of Minneapolis

Azqueta-Gavaldon A (2017) Developing news-based economic policy uncertainty index with unsupervised machine learning. Econ Lett 158:47–50

Azzimonti M (2019) Does partisan conflict deter FDI inflows to the US? J Int Econ 120:162–178

Bachmann R, Elstner S, Sims E (2013) Uncertainty and economic activity: evidence from business survey data. Am Econ J Macroecon 5(2):217–224

Bai J, Ng S (2002) Determining the number of factors in approximate factor models. Econometrica 701:191–221

Baker M, Foley CF, Wurgler J (2009) Multinationals as arbitrageurs: the effect of stock market valuation on foreign direct investment. Rev Financ Stud 22:337–369

Baker S, Bloom N, Davis SJ, Wang X (2013) A Measure of economic policy uncertainty for China, University of Chicago Working Paper

Baker SR, Bloom N, Davis SJ (2016) Measuring economic policy uncertainty. Quart J Econ 131(4):1593–1636

Balta N, Fernández V, Ruscher E (2013) Assessing the impact of uncertainty on consumption and investment. Eur Comm Q Rep Euro Area 12(2):7–16

Basu S, Bundick B (2017) Uncertainty shocks in a model of effective demand. Econometrica 85:937–958

Benigno G, Benigno P, Nisticó (2012) Risk, monetary policy and the exchange rate. NBER Macroecon Annu 26(1):247–309

Berger T, Grabert S, Kempa B (2016) Global and country-specific output growth uncertainty and macroeconomic performance. Oxf Bull Econ Stat 78(5):694–716

Bernanke BS (1983) Irreversibility, uncertainty and cyclical investment. Quart J Econ 98(1):85–106

Bhattarai S, Chatterjee A, Park WY (2020) Global spillover effects of US uncertainty. J Monet Econ 14:71–89

Blei DM, Ng AY, Jordan MI (2003) Latent Dirichlet allocation. J Mach Learn Res 3:993–1022

Blei DM (2012) Probabilistic topic models. Commun ACM 55(4):77–84

Bloom N (2009) The impact of uncertainty shocks. Econometrica 77(3):623–685

Bonciani D, Ricci M (2018) The global effects of global risk and uncertainty. European Central Bank Working Paper No. 2179

Born B, Pfeifer J (2014) Policy risk and the business cycle. J Monet Econ 68:68–85

Busse M, Hefeker C (2007) Political risk, institutions and foreign direct investment. Eur J Polit Econ 23(2):397–415

Caggiano G, Castelnuovo E, Groshenny N (2014) Uncertainty shocks and unemployment dynamics: an analysis of post-WWII U.S. recessions. J Monet Econ 67:78–92

Caggiano G, Castelnuovo E, Figueres JM (2017) Economic policy uncertainty and unemployment in the United States: a nonlinear approach. Econ Lett 151:31–34

Caggiano G, Castelnuovo E, Figueres JM (2020) Economic policy uncertainty spillovers in booms and busts. Oxf Bull Econ Stat 82:125–155

Caldara D, Fuentes-Albero C, Gilchrist S, Zakrajs̆ek E (2016) The macroeconomic impact of financial and uncertainty shocks. Eur Econ Rev 88:185–207

Carrière-Swallow Y, Cèpedes LF (2013) The impact of uncertainty shocks in emerging countries. J Int Econ 90:316–325

Carriero A, Clark TE, Marcellino M (2018a) Measuring uncertainty and its impacts on the economy. Rev Econ Stat 100(5):799–815

Carriero A, Clark TE, Marcellino M (2018b) Endogenous Uncertainty. Federal Reserve Bank of Cleveland Working Paper No. 18-05

Carriero, A., Clark, T.E., Marcellino, M., 2019. The identifying information in vector autoregressions with time-varying volatilities: An application to endogenous uncertainty. Federal Reserve Bank of Cleveland Working Paper 18-05

Carroll CD (1997) Buffer-stock saving and the life cycle/permanent income hypothesis. Q J Econ 112(1):1–55

Cascaldi-Garcia D, Galvao AB (2018) News and Uncertainty Shocks. International Finance Discussion Papers 1240

Castelnuovo E, Tran TD (2017) Google it up! A google trends-based uncertainty index for the United States and Australia. Econ Lett 161:149–153

Cerda R, Silva A, Valente J (2018) Impact of economic uncertainty in a small open economy: the case of Chile. Appl Econ 50(26):2894–2908

Cesa-Bianchi A, Pesaran MH, Rebucci A (2018) Uncertainty and economic activity: a multi-country perspective. NBER Working Paper No. w24325

Chang J, Gerrish S, Wang C, Boyd-Graber J, Blei DM (2009) Reading tea leaves: how humans interpret topic models. In: Proceedings of the 22nd international conference on neural information processing systems, pp 288–296

Chatterjee P (2018) Asymmetric impact of uncertainty in recessions—are emerging countries more vulnerable? Stud Nonlinear Dyn Econom 23(2):1–27

Chatterjee P (2019) Uncertainty shocks, financial frictions and business cycle asymmetries across countries. University of New South Wales, mimeo

Cheng CHJ (2017) Effects of foreign and domestic economic policy uncertainty shocks on South Korea. J Asian Econ 51:1–11

Christiano LJ, Motto R, Rostagno M (2014) Risk shocks. Am Econ Rev 104(1):27–65

Choi S, Loungani P (2015) Uncertainty and unemployment: effects of aggregate and sectoral channels. J Macroecon 46:344–358

Colombo V (2013) Economic policy uncertainty in the US: does it matter for the Euro area? Econ Lett 121:39–42

Creal DD, Wu JC (2017) Monetary policy uncertainty and economic fluctuations. Int Econ Rev 58(4):1317–1354

Cuaresma JC, Huber F, Onorante L (2019) The macroeconomic effects of international uncertainty. European Central Bank Working Paper No. 2302

Davis SJ (2016) An index of global economic policy uncertainty. NBER Working Paper No. 22740

Favero C, Giavazzi F (2008) Should the Euro area be run as a closed economy? Am Econ Rev 98(2):138–145

Fernàndez-Villaverde J, Guerrón-Quintana P, Rubio-Ramírez JF, Uribe M (2011) Risk matters: the real effects of volatility shocks. Am Econ Rev 101(6):2530–61

FOMC (Federal Open Market Committee) (2009) Minutes of the Federal Open Market Committee, December 15–16, 2009

Forbes KJ, Warnock FE (2012) Capital flow waves: surges, stops, flight, and retrenchment. J Int Econ 88(2):235–251

Forbes K (2016) Uncertainty about uncertainty. Technical Report, Speech to be given by Kristin Forbes, External MPC Member, at J.P. Morgan Cazenove Best of British Conference, London

Gilchrist S, Sim JW, Zakrajs̆ek E (2014) Uncertainty, financial frictions and investment dynamics. NBER Working Paper No. 20038

Griffiths TL, Steyvers M (2004) Finding scientific topics. Proc Natl Acad Sci 101:5228–5235

Guglielminetti E (2016) The labor market channel of macroeconomic uncertainty. Bank of Italy Working Paper No. 1068

Haddow A, Hare C, Hooley J, Shakir T (2013) Macroeconomic uncertainty: what is it, how can we measure it and why does it matter? Bank Engl Q Bull 53(2):100–109

Handley K (2014) Exporting under trade policy uncertainty: theory and evidence. University of Michigan Working Paper

Handley K, Limão N (2012) Trade and investment under policy uncertainty: theory and firm evidence. NBER Working Paper No. 17790

Huang Z, Tong C, Qui H, Shen Y (2018) The spillover of macroeconomic uncertainty between the US and China. Econ Lett 171(5):123–127

Husted L, Rogers J, Sun B (2020) Monetary policy uncertainty. J Monet Econ 115:20–36

Hlaing SW, Kakinaka M (2019) Global uncertainty and capital flows: any difference between foreign direct investment and portfolio investment? Appl Econ Lett 3

IMF (2013) Hopes, realities, risks. World Economic Outlook, April 2013

Jurardo K, Ludvigson SC, Ng S (2015) Measuring uncertainty. Am Econ Rev 105(3):1177–1216

Julio B, Yook Y (2016) Policy uncertainty, irreversibility and cross-border flows of capital. J Int Econ 103:13–26

Kang W, Ratti RA, Vespignani J (2019) Impact of global uncertainty on the global economy and large developed and developing economies. Appl Econ 52:2392–2407

Kilian L (1998) Small-sample confidence intervals of impulse response functions. Rev Econ Stat 80(2):218–230

Kimball MS (1990) Precautionary saving in the small and in the large. Econometrica 58(1):53–73

Knotek ES, Khan S (2011) How do households respond to uncertainty shocks? Kansas City Federal Reserve Board Economic Review

Kozeniauskas N, Orlik A, Veldkamp L (2018) What are uncertainty shocks? J Monet Econ 100:1–15

Larsen VH (2021) Components of uncertainty. Int Econ Rev (forthcoming)

Leduc S, Liu Z (2016) Uncertainty shocks are aggregate demand shocks. J Monet Econ 82:20–35

Londono JM, Ma S, Wilson BA (2019) Quantifying the impact of foreign economic uncertainty on the US economy. FEDS Notes

Luangaram P, Sethapramote Y (2020) Capital flows and political conflicts: Evidence from Thailand. Econ Peace Secur J 15(2):83–100

Ludvigson SC, Ma S, Ng S (forthcoming) Am Econ J Macroecon

Luk P (2017) Global banks, International business cycles and monetary policy. Hong Kong Baptist University Working Paper

Luk P, Cheng M, Ng P, Wong K (2017) Economic policy uncertainty spillovers in small open economies: the case of Hong Kong

McDonald R, Siegel D (1986) The value of waiting to invest. Q J Econ 101(4):707–727

Meinen P, Roehe O (2017) On measuring uncertainty and its impact on investment: cross-country evidence from the Euro area. Eur Econ Rev 92:161–179

Miescu MS (2019) Uncertainty shocks in emerging economies: a global to local approach for identification. Lancaster University Economics Working Paper Series No. 2019/017

Moore A (2017) Measuring economic uncertainty and its effects. Econ Rec 93:550–575

Mumtaz H (2018) Does uncertainty affect real activity? Evidence from state-level data. Econ Lett 167:127–130

Mumtaz H, Theodoridis K (2017) Common and country specific economic uncertainty. J Int Econ 105(C):205–216

Mumtaz H, Musso A (2018) The evolving impact of global, region-specific and country-specific uncertainty. European Central Bank Working Paper No. 2147

Mumtaz H, Surico P (2018) Policy uncertainty and aggregate fluctuations. J Appl Econom 33(3):319–331

Mumtaz H, Theodoridis K (2015) The international transmission of volatility shocks: an empirical analysis. J Eur Econ Assoc 13(3):512–533

Novy D, Taylor AM (2014) Trade and uncertainty, NBER Working Paper No. 19941

Orlik A, Veldkamp L (2014) Understanding uncertainty shocks and the role of black swans. NBER Working Paper No. w20445

Phillips KL, Spencer DE (2011) Bootstrapping structura VARs: avoiding a potential bias in confidence intervals for impulse response functions. J Macroecon 33(4):582–594

Razin A, Sadka E, Yuen C (1998) A pecking order of capital flows and international tax principles. J Int Econ 44:45–68

Redl C (2017) The impact of uncertainty shocks in the United Kingdom. Bank of England Working Paper No. 695

Rey H (2013) Dilemma not trilemma: the global financial cycle and monetary policy independence. Federal Reserve Bank of Kansas City Economic Policy Symposium

Ricco G, Callegari G, Cimadomo J (2016) Signals from the government: policy uncertainty and the transmission of fiscal shocks. J Monet Econ 82:107–118

Rich R, Tracy J (2010) The relationships among expected inflation, disagreement and uncertainty: evidence from matched point and density forecasts. Rev Econ Stat 92(1):200–207

Rossi B, Sekhposyan T (2015) Macroeconomic uncertainty indices based on nowcast and forecast error distributions. Am Econ Rev (Paper and Proceedings) 105(5):650–655

Scotti C (2016) Surprise and uncertainty indexes: real-time aggregation of real-activity macro surprises. J Monet Econ 82:1–19

Sims C, Stock J, Watson M (1990) Inference in linear time series models with some unit roots. Econometrica 58(1):113–144

Wallach HM, Murray I, Salakhutdinov R, Mimno D (2009) Evaluation methods for topic models. In: Proceedings of the 26th annual international conference on machine learning. ACM, Harvard, pp 1105–1112

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

We would like to thank Patcharaporn Leepipatpiboon and Chaitat Jirophat for excellent research assistance. We also appreciate insightful and constructive comments by two anonymous referees. The views expressed in this paper are of the authors and do not necessarily reflect those of the Bank of Thailand.

Appendices

Appendix A: Model-based uncertainty measure

The JLN approach estimates uncertainty from a large number of macroeconomic and financial time series based on a diffusion index and stochastic volatility models. We apply the JLN approach to construct macroeconomic and financial uncertainty indices for Thailand. In doing so, we first let \(y^C_{jt}\) be a variable in either the macro or financial category. Its forecast, \(E[y^C_{jt+h}|I_t]\) can be estimated from the following factor augmented forecasting model:

where \(\phi _j^y(L), \gamma _j^F(L), \gamma _j^W(L)\) are finite-order polynomials. The factors \({\hat{\mathbf{F}}_t}\) are drawn from the information set \(I_t\) which is approximated by the full dataset which contains both macroeconomic and financial time series variables.Footnote 16\(\mathbf{W_t }\) contains additional predictors that are meant to capture possible nonlinearities such as the squares of the first component of \({\hat{\mathbf{F}}_t}\). In the model, the prediction error for \(y^C_{jt+1}, {\hat{\mathbf{F}}_t}, \mathbf{W_t }\) are permitted to have time-varying volatility \(\sigma ^y_{jt+1}, \sigma ^F_{kt+1}, \sigma ^W_{lt+1}\), respectively, which generates time-varying uncertainty in the overall series \(y^C_{jt}\).

From Eq (1), we compute the forecastable component \(E[y^C_{jt+h}|I_t]\) which form the basis of our uncertainty measures. More specifically, we calculate the forecast error as \(V^{y^C}_{jt+h} = y^C_{t+h} - E[y^C_{jt+h}|I_t]\), where the conditional volatility of this forecast error \(E[(V^{y^C}_{jt+h})^2|I_t]\) is then generated based on a parametric stochastic volatility model for the one-step-ahead prediction errors in \(y^C_{jt}\) and the factors. Then, using a recursive method, we can estimate \(E[(V^{y^C}_{jt+h})^2|I_t]\) for future horizons \(h>1\). As discussed in JLN, the stochastic volatility modeling approach allows for shocks to the second moment of a variable to be independent from the first moment, consistent with theoretical models of uncertainty which presumes the existence of an uncertainty shock that independently affects \(y_j\).

Finally, uncertainty for the variable \(y^C_{jt} \) at horizon h can be computed as:

which measures uncertainty as the conditional volatility of the purely unforecastable component of the h-step-ahead realization of each underlying macroeconomic and financial time series based on available information at time t. We follow JLN and assume equal weights \(w_j=\frac{1}{N_C}\) to arrive at the aggregate uncertainty measure:Footnote 17

Based on Eq. (3), we compute the macroeconomic and financial uncertainty measures by aggregating the conditional variances of the unforecastable components over variables that belong to the either macroeconomic or financial categories. For both measures, we compute uncertainty for the forecasting horizons \(h=4\), but also consider various other horizons for robustness checks.Footnote 18

The underlying dataset to construct Thai economic uncertainty indices comprises of monthly macroeconomic and financial data obtained from the Bank of Thailand and the Stock Exchange of Thailand databases over the 2002M1–2019M12 sample. We choose to construct the series based on monthly data for a wider information set and then construct quarterly uncertainty indices by taking within-quarter averages. In the full dataset, we have 199 macroeconomic series that represent broad categories that describe the macroeconomy (Groups 1–10) and 22 financial series (Group 11) as listed in Table 5. In the table, each series has one of the following transformation codes which are applied to the data series to ensure stationarity:

Macroeconomic time series transformations

-

1:

\(X_{it} = X^A_{it}\)

-

2:

\(X_{it} = X^A_{it} - X^A_{it-1}\)

-

3:

\(X_{it} = \Delta ^2 X^A_{it}\)

-

4:

\(X_{it} = ln(X^A_{it})\)

-

5:

\(X_{it} = ln(X^A_{it}) - ln(X^A_{it-1} )\)

-

6:

\(X_{it} = \Delta ^2 lnX^A_{it}\)

-

7:

\(X_{it} = (X^A_{it}-X^A_{it-1})/X^A_{it-1}\)

where \(X_{it}\) denotes the transformed variable i and \(X^A_{it}\) is the actual or raw data series. Note that we use the notation \(\Delta = 1-L\) and \(LX_{it} = X_{it-1}\).

Financial time series transformations

For the first five financial time series with transformation code 8, we follow the method as described below.

-

\(D\_log(DIV): \Delta logD^*_t\)

-

\(D\_log(P): \Delta logP_t\)

-

\(D\_DIVreinvest: \Delta logD^{re,*}_t\)

-

\(D\_Preinvest: \Delta logP^{re,*}_t\)

-

d-p: \( log(D^*_t)-log(P_t)\)

Note that to obtain the dividend and price series, \((D^*_t\) and \(P_t)\), we first construct the return series with dividends (\(RETD_t\)) and excluding dividends (\(RETX_t\)) as: \(RETD_t = \frac{P_{t=1}+D_{t+1}}{P_t}\) and \(RETX_t=\frac{P_{t+1}}{P_t}\), and produce a normalized price series based on the recursive rule: \(P_0=1, P_t=P_{t-1}RETX_t\). A dividend series can then be constructed as: \( D_t =P_{t-1}(RETD_t - RETX_t) \) where \(D^*_t = (D_t+D_{t-1} + D_{t-2} + D_{t-3})\).

For dividends and prices under reinvestment, \((D^{re*}_t\) and \(P^{re*}_t)\), we use the recursion \(P^{re}_0 =1, P^{re}_t = P_{t-1} RETD_t\). Then, dividends under reinvestment can be defined as \(D_t^{re} = P^{re}_{t-1}(RETD_t - RETX_t)\) where as before, \(D^{re*}_t = (D_t^{re} + D^{re}_{t-1} + D^{re}_{t-2} + D^{re}_{t-3})\).

Finally, for the remaining 17 financial time series which are industry portfolios, the portfolio returns are constructed from the price and dividend yield series as follows:

Appendix B: News-based uncertainty measure

To construct topic-based uncertainty measures, we adopt Azqueta-Gavaldon (2017) by employing the latent Dirichlet allocation (LDA) method, the most popular topic-modeling approach that has been developed by Blei et al. (2003) to help uncover the underlying topics in the Thai-language newspapers. The steps that we follow are as outlined below:

Number of topics and perplexity. Note Validation perplexity is based on the log probabilities of randomly selected articles in a 10% test set. Details on calculations can be found in Wallach et al. (2009)

-

(i)

Select articles in the economics and business section that contain any of the following keywords: {“uncertain(ty),” “delayed,” “conflict,” “crisis,” “postpone,” “procrastinate,” “confused,” “unsure,” “bankrupt,” “unclear,” “risk(y),” “halted,” “ambiguous”}.

-

(ii)

Screen out articles that are too short (less than 50 words) or too long (more than 1000 words), which leaves us with a total of remaining 91,400 news articles. Based on our reading in the Thai newspapers, we find that very short articles often contain uninformative news including advertisement and gossip sections while very long articles contain too many different topics that could potentially introduce noise into the estimation process. Note that, on this issue, other refinement process can be applied. For example, Husted et al. (2020) construct monetary policy uncertainty using proximity refinement by restricting uncertainty words to be within 5-20 words of the phrase ‘federal reserve’ or ‘monetary policy’.

-

(ii)

Apply standard preprocessing by removing stop words and punctuation, lemmatization and stemming.

-

(iii)

Employ the LDA approach to uncover underlying topics. The LDA assumes a generative process with the following joint distribution:

$$\begin{aligned} p(\theta , z, w| \alpha , \beta ) = p(\theta |\alpha ) \prod _{n=1}^N p(z_n|\theta ) p(w_n|z_n,\beta ), \end{aligned}$$where each document has a multinomial distribution \(\theta \) of topics. A document’s topic distribution is randomly sampled from a Dirichlet distribution with \(\alpha \) as a parameter governing the concentration, \(\beta = \{\beta _1,...,\beta _k\}\) as the topic-word probabilities of K topics, and \(z=\{z_1,...,z_N\}\) and \(w=\{w_1,...,w_N\}\) are sets of N topics and words, respectively. In this study, we set \(\alpha = 50/K\) and \(\beta = 0.1\) as suggested by Griffiths and Steyvers (2004) and compare the goodness of fit of models with different values of K. The goodness of fit for each model is based on calculating the perplexity value as proposed by Wallach et al. (2009).Footnote 19

Figure 13 shows the model’s evaluation based on the perplexity value for K between 5 and 200. We find that the goodness of fit improves monotonically with a larger K. Therefore, we also need to consider the interpretability of the topics derived from the model based on our own subjective judgment. Too few topics can produce results that are too broad, while selecting too many topics can lead to too detailed and redundant topics. In our case, we find that the topics become very specific and semantically less meaningful when K is above 50. Thus, we choose \(K = 50\) which yields the most interpretable result. Applying a subjective judgment for K is a valid approach that has also been carried out by Larsen (2021), in which he picked \(K=80\) to construct measures of economic uncertainty using the LDA method for Norway. In addition, as cited in Larsen (2021), Chang et al. (2009) conclude that “practitioners developing topic models should thus focus on evaluations that depend on real-world task performance rather than optimizing likelihood-based measures” (p. 296).

-

(iv)

Construct the uncertainty index for each topic based on the number of articles describing uncertainty for each topic. More specifically, we first label each article d with its most likely topic (the topic with the highest probability \(\theta _d\)). The index is then the estimated topic proportion for each topic within a quarter.

Appendix C: Impulse response analysis of domestic uncertainty subcomponents

See Figs. 14, 15, 16, 17, 1819, 20, 21, 22, 23, 24 and 25.

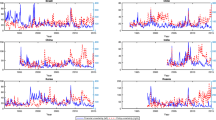

Impulse responses of macroeconomic variables to global uncertainty and domestic macroeconomic uncertainty shocks (production and growth outlook). Note Plotted are the impulse responses to global and domestic macroeconomic uncertainty shocks. Shaded regions correspond to 68% standard error bands

Impulse responses of macroeconomic variables to global uncertainty and domestic macroeconomic uncertainty shocks (commodity prices and agricultural products). Note Plotted are the impulse responses to global and domestic macroeconomic uncertainty shocks. Shaded regions correspond to 68% standard error bands

Impulse responses of macroeconomic variables to global uncertainty and domestic financial uncertainty shocks (capital markets). Note Plotted are the impulse responses to global and domestic macroeconomic uncertainty shocks. Shaded regions correspond to 68% standard error bands

Impulse responses of macroeconomic variables to global uncertainty and domestic financial uncertainty shocks (credit markets). Note Plotted are the impulse responses to global and domestic macroeconomic uncertainty shocks. Shaded regions correspond to 68% standard error bands

Impulse responses of macroeconomic variables to global uncertainty and domestic monetary policy uncertainty shocks. Note Plotted are the impulse responses to global and domestic macroeconomic uncertainty shocks. Shaded regions correspond to 68% standard error bands

Impulse responses of macroeconomic variables to global uncertainty and domestic fiscal uncertainty shocks. Note Plotted are the impulse responses to global and domestic macroeconomic uncertainty shocks. Shaded regions correspond to 68% standard error bands

Impulse responses of financial variables to global uncertainty and domestic macroeconomic uncertainty shocks (production and growth outlook). Note Plotted are the impulse responses to global uncertainty and domestic financial uncertainty shocks. Shaded regions correspond to 68% standard error bands

Impulse responses of financial variables to global uncertainty and domestic macroeconomic uncertainty shocks (commodity prices and agricultural products). Note Plotted are the impulse responses to global uncertainty and domestic financial uncertainty shocks. Shaded regions correspond to 68% standard error bands

Impulse responses of financial variables to global uncertainty and domestic financial uncertainty shocks (capital markets). Note Plotted are the impulse responses to global uncertainty and domestic financial uncertainty shocks. Shaded regions correspond to 68% standard error bands

Impulse responses of financial variables to global uncertainty and domestic financial uncertainty shocks (credit markets). Note Plotted are the impulse responses to global uncertainty and domestic financial uncertainty shocks. Shaded regions correspond to 68% standard error bands

Impulse responses of financial variables to global uncertainty and domestic monetary policy uncertainty shocks. Note Plotted are the impulse responses to global uncertainty and domestic financial uncertainty shocks. Shaded regions correspond to 68% standard error bands

Impulse responses of financial variables to global uncertainty and domestic fiscal uncertainty shocks. Note Plotted are the impulse responses to global uncertainty and domestic financial uncertainty shocks. Shaded regions correspond to 68% standard error bands

Rights and permissions

About this article

Cite this article

Apaitan, T., Luangaram, P. & Manopimoke, P. Uncertainty in an emerging market economy: evidence from Thailand. Empir Econ 62, 933–989 (2022). https://doi.org/10.1007/s00181-021-02054-y

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00181-021-02054-y